Heritage Pool Supply Group — is it following POOL's footprint or building independently?

Emphatically following. Heritage is shadowing POOLCORP's footprint, not building independently. 107 of 163 Heritage branches (65.6%) sit within 5 miles of an existing POOL sales center; 84% are within 10 miles. The median Heritage branch is 2.78 miles from the nearest POOL location. Heritage operates in 37 states — every one of which POOL also serves — and there are zero Heritage-only states.

Source data: dashboards/pool_locations/heritage_overlap_metrics.json |

Findings doc: dashboards/pool_locations/HERITAGE_OVERLAP.md |

Scraped May 20, 2026 via scrape_heritage_xhr.py from the HPSG /api/branchList/features/ endpoint

Heritage vs POOL — interactive overlay

● POOL locations (424) | ▲ Heritage locations (163) | toggle layers with the top-right control · click any marker for details

Distance from each Heritage branch to nearest POOL

Right-skew is dramatic: more than 100 of 163 branches sit within 5 miles. The few >50mi outliers are pure white-space (8 branches: Laredo TX, Midland TX, Saginaw MI, Maui HI, etc.).

State coverage — both / POOL-only / neither

POOL-only states (4): OR (5 br), NM (1), ND (1), WV (1) = 8 branches total. Heritage-only states: 0. 10 states (mostly low-pool-density rural + AK/DC) have neither.

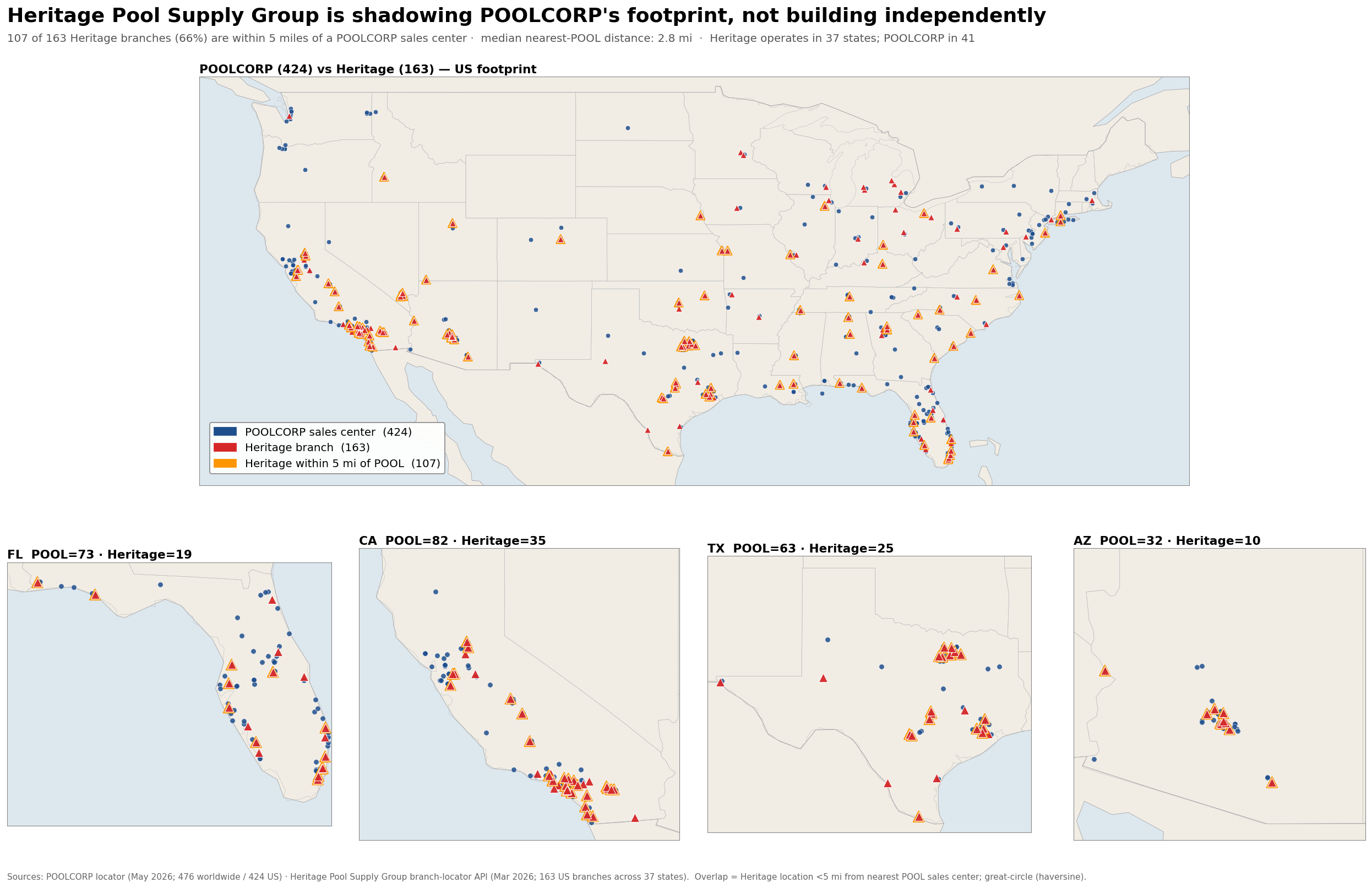

Sand State zoom (FL/CA/TX/AZ)

Heritage = 89 of 163 branches (55%) concentrate in the Sand States. 74% of those 89 are within 5 mi of a POOL — i.e. the share-shift threat is structurally aimed at POOL's most valuable geographic concentration. CA gap is widest at 82 POOL vs 35 Heritage (43% coverage ratio).

Heritage brand mix (163 branches)

Heritage Pool Supply is the consolidated front-end brand (134 / 163 = 82%). The corporate-structure §2 from HERITAGE_CONTEXT.md lists ~12 brands; most appear consolidated into HPS in the API. Recreonics (1 in API vs national commercial network per acquisition press release) is under-represented — may operate under separate portal.

State-by-state coverage detail

| State | POOL | Heritage | H/P ratio | Status |

|---|

Sortable rendering. Heritage/POOL ratio shows where Heritage has caught up most aggressively: HI is the standout (Heritage 4 vs POOL 2 = 200%) but POOL effectively wasn't there before the Island Pool & Spa acquisition. MI 5 vs 3, OH 5 vs 4, OK 4 vs 4 are other Heritage-overweight states. Heritage is meaningfully under-indexed in NY, NJ, NV vs POOL.

Static map (with Sand State insets)

Generated by build_heritage_map.py. 1 US panel + 4 Sand-State zoom insets. POOL blue dots, Heritage red triangles, orange rings around within-5mi overlaps.

📈 Investment implications & share-shift thesis

- The headwind is broad-based, not isolated. Heritage now has presence within 10 miles of POOL in 84% of POOL's network. POOLCORP's "same-store-sales (SSS) drag from Heritage" headline cannot be dismissed as a 1–2 market issue — every greenfield Heritage opens should be modeled as direct SSS pressure on the nearest POOL branch.

- No TAM expansion left for Heritage in 99% of cases. Only 8 of 163 Heritage branches (4.9%) are truly white-space (>50mi from any POOL). Heritage's growth model is share-take, not market creation.

- The Sand State threat is concentrated where it hurts most. 74% of Heritage's 89 SS branches are within 5 mi of a POOL. POOL's 53% of FY25 sales from CA/FL/TX/AZ (10-K) is the most exposed slice. CA is the largest gap (POOL 82 vs Heritage 35 = 43% Heritage coverage) and the highest-revenue state — meaningful runway for Heritage greenfields in CA without TAM expansion.

- The 4 POOL-only states are immaterial. OR, NM, ND, WV combined = 8 POOL branches. Heritage's choice not to enter is rational — these are low-pool-density markets.

- Confirms the duopoly structure (task #10). The wholesale 2-step pool distribution market is now a POOL+Heritage duopoly:

- POOL US: 424 branches, ~62% share, ~$4.6B revenue

- Heritage: 163 branches, ~16% share, ~$1.2B revenue

- All other regional independents: ~100 branches, ~4% share, ~$300M (per Pool_Distributors_Data.xlsx > Chain_vs_Indep)

- No third national competitor at Heritage's scale exists. POOL is rolling up the tail (Shoreline 2024, Swimline 2024, Great Plains 2025).

- Map this back to the 1Q26 commentary. Arvan's IDay 2024 framing was "no new competition, just a roll-up" — that quote is increasingly hard to defend with 65.6% of Heritage branches inside 5 miles of POOL and Heritage gaining share per channel checks. Watch for an updated articulation at the May 12, 2026 Investor Day follow-up or Q2 print (Jul 23).

🌐 Public catalog asymmetry — Heritage Pool Plus is open-web, POOL360 is dealer-gated

Recon of every POOL- and Heritage-controlled e-commerce property (May 2026) found a structural go-to-market divergence at the catalog tier: Heritage Pool Plus exposes a ~74,000-URL public Magento catalog (product names, photos, specs, categories — no login wall), while POOL's flagship digital channels (POOL360, SCP, Superior, NPT) gate the entire catalog behind dealer authentication.

⚠ Important caveat added May 2026: the pricing tier shows no asymmetry. A follow-up scrape of 78 Heritage Pool Plus product pages across 7 strategic SKU buckets (VS pumps, heaters, filters, salt, automation, robotic) found 0 of 78 products show public dollar prices; every page references the HeritagePro contractor program / wholesale tier. See the dedicated Pricing Competitiveness section below — both sides gate pricing.

Site-by-site public-catalog audit

| Site | Owner | Public sitemap? | Public catalog? | URLs / products |

|---|---|---|---|---|

| heritagepoolplus.com | Heritage | Yes (5 sub-sitemaps) | YES — no login | 73,980 URLs |

| recreonics.com | Heritage (commercial) | Yes (4 product sitemaps) | YES — no login | 3,218 products · 272 categories |

| heritagepoolsupplygroup.com | Heritage (corp) | Yes | N/A (corporate) | ~50 pages |

| pool360.poolcorp.com | POOL | No | NO — dealer auth | Gated (15% of FY25 net sales) |

| scppool.com | POOL | No public sitemap | NO | Next.js, no product feed exposed |

| superiorpoolproducts.com | POOL | No | NO | — |

| nptpool.com | POOL | 1 sitemap (1 URL) | NO | Dealer/contractor finder only (/api/dealers public — 106 FL contractors) |

| texaspoolsupply.com | Heritage (local brand) | — | Redirects | → HPSG "South Region" page |

| poolbuilderssupply.com | Heritage (local brand) | — | Redirects | → HPSG "Southeast Region" page |

| aquafinity.com | Heritage (commercial) | Yes | No (marketing site) | 142 pages |

| belaquapoolsupply.com | Heritage (local brand) | — | — | PARKED at GoDaddy despite active brand (2022 NJ greenfield) |

| mtpooldistributors.com | Heritage (Nov 2025 acq) | No | — | Minimal (post-acq integration) |

Source: recon scrape May 2026, dashboards/pool_locations/raw/ecommerce/deep_recon.json + SCRAPE_FINDINGS.md. All Heritage Pool Plus URLs available as a 7.5 MB seed file (heritagepoolplus_all_sitemap_urls.txt) for any future targeted SKU-bucket extraction.

The two readings — what this divergence means

Open catalog = SEO/search visibility for product queries, lower friction for DIY-homeowner cross-sells and sub-dealer prospecting. Heritage is courting the digital-search funnel that POOL has chosen not to compete in. Consistent with the Hayward expert's read that Heritage is "sharpened their pencil" on pricing and culture — public pricing is the logical extension.

Publishing prices openly weakens trade-only pricing differentiation — Heritage's pro customers see the same prices a consumer sees. POOL360's gated stance deliberately preserves the "professional-only" trade discount, matching Arvan's repeated "we serve the pool pro, not the homeowner" framing. If Heritage's open-catalog channel cannibalizes its own trade margins, the share-shift narrative could partially reverse as Heritage's gross margin compresses.

Heritage's catalog is publicly inspectable — pricing, availability, brand mix, SKU breadth, all observable without dealer credentials. This makes Heritage's gross margin materially easier to model than POOL's: targeted weekly scrapes of a 1,000-2,000 SKU bucket (e.g., variable-speed pumps, premium plaster finishes) would yield a real-time pricing/inventory time series. POOL has no equivalent visibility into its own catalog without dealer credentials, let alone Heritage's.

💡 Investment implications — the e-commerce dimension

- Heritage's 74K-URL public catalog is a genuine moat and a vulnerability. Moat: search visibility, sub-dealer leads, DIY traffic. Vulnerability: open prices erode the trade-pricing differentiation that distributors live on. Net effect depends on whether Heritage holds margin while POOL holds trade share.

- POOL360's 15% of FY25 net sales is dealer-only traffic — a fundamentally different mix from Heritage Pool Plus's open-web visitors. The 15% should NOT be compared to Heritage Pool Plus directly. POOL's POOL360 is incremental dealer ordering efficiency; Heritage Pool Plus is a top-of-funnel customer-acquisition channel.

- The Bel-Aqua parked-domain tell. An "active" Heritage brand (Lakewood NJ 2022 greenfield per press releases) with a domain parked at GoDaddy suggests the multi-brand strategy is more nominal than operational at the web layer — physical branches are real but local-brand digital presence is patchy.

- Future-extension paths if the user wants this monitored:

- Targeted SKU-bucket pricing scrape (1k-2k Heritage Pool Plus products in a chosen category) → gross-margin model

- Recurring weekly in-stock/out-of-stock ratio for Heritage → supply-chain proxy with no POOL equivalent

- Cross-link Heritage catalog by acquired-brand mix (HPS / Aquafinity / Recreonics / etc.) to validate the 12-brand corporate-structure footprint

💰 Pricing Competitiveness — Are POOL and Heritage discounting to win contractors?

YES — but the competition is structurally invisible from outside. Heritage is actively undercutting POOL on contractor pricing per multiple independent sources (Hayward ex-Pres, TX builder, POOL CFO own acknowledgment). The mechanism is volume rebates + face-to-face quotes, both of which are off-invoice and gated behind dealer auth on every retailer's website. Industry-wide MAP enforcement removes any public-pricing window for cross-channel comparison.

🎙 Three-source qualitative evidence

All three sources independently describe Heritage as the price-aggressive party. Full quotes + page citations on the Quotes & Channel Checks tab.

🔍 What we tried to observe directly — and why it's gated

Two scraper runs in May 2026 attempted to extract public SKU-level pricing. Findings:

| Source | Public pricing? | What we saw |

|---|---|---|

| Heritage Pool Plus 78 products · 7 categories | No | 0 of 78 products show $-amounts in HTML. Every page mentions HeritagePro (4×) and Wholesale (3×) tier login. |

| POOL360 / SCP / Superior / NPT | No | Catalog itself is gated behind dealer auth. No prices visible to anonymous users. |

| Pinch A Penny POOL-owned retail; consumer proxy | No | Homepage shows 0 $-prices. Sign-in CTA on every product page. |

| Leslie's (LESL) Public consumer benchmark | Mostly no | Even the IntelliFlo3 VSF (~$1,500 pump) product page shows only accessory prices ($19.99, $7.95) — the actual pump price is gated. MAP badge on the page. |

This is the MAP-enforcement layer. Pentair, Hayward, and Zodiac all require their retailers to honor Minimum Advertised Pricing rules. Display of below-MAP prices online — even for legitimate sales — risks losing the line. Both POOL and Heritage are bound to this. The actual selling price (which is what the experts say differs) only appears in the cart after login OR in a face-to-face / phone quote. There is no public window into the pricing battleground.

⚙ How the competition actually works (per Hayward ex-Pres)

- Manufacturer list price — Pentair / Hayward / Zodiac publish a list price (the MAP).

- Distributor cost — undifferentiated between POOL and Heritage. Quote: "The day-in, day-out acquisition cost of the goods is undifferentiated."

- Volume rebate — manufacturer pays the distributor a double-digit % rebate based on annual purchasing volume, growth, strategic alignment. POOL's scale advantage shows up HERE, not in invoice cost.

- Distributor contractor price — distributor sells to contractor at some markup above cost. THIS is where Heritage "sharpens the pencil" — accepts a thinner markup on the same MAP-listed product to take share.

- Contractor invoice to homeowner — built on the distributor cost + contractor margin. Homeowner never sees the rebate math.

Implication: Heritage's price advantage is funded out of margin, not cost structure. If they hold this aggressive posture they take share but compress gross margin. If they relent they keep margin but lose the share-shift narrative. This is the structural tension to watch in any Heritage P&L disclosure (rare today — Heritage is buried inside SRS Distribution / Home Depot reporting).

📐 What we CAN observe (the proxies)

- POOL gross margin trajectory — FY25 GM was 29.7% (flat YoY). Q1 26 was 29.0% (-20 bps). Mgmt explicitly cites product mix & early-buy as drivers, NOT competitive pricing pressure. If Heritage were forcing POOL to cut prices, we'd see it here first.

- POOL pricing contribution to growth — Q1 26 = ~3% pricing (1-2% normal vendor cost pass-through + 1% lapping of FY25 tariff actions). Stable. No price war signature.

- Heritage 65.6% within-5-mi overlap (Tab 4 above) — the share-shift mechanism is local-presence-driven first; pricing is the secondary lever once Heritage is in the market.

- Heritage's same brand mix as POOL — Pentair, Hayward, Zodiac, Maytronics carried by both. No selection moat to compete on. Price + relationship + branch density are the only levers, and Heritage is pulling all three.

- TX builder's spend shift — "65% with POOL right now, but it is changing" → revised to ~20% incremental purchasing with POOL = a directional signal of the customer-level dollars moving without any of us seeing the per-SKU prices that drove it.

🛠 Future extension paths (if user wants to push deeper)

- HeritagePro account creation — sign up as a real contractor (if Unison-affiliated entity qualifies) to access the gated Heritage Pool Plus pricing layer. Same idea for POOL360. Most direct path but requires legitimate trade credentials and crosses a different ethical line (using a research account to extract competitive pricing).

- Manufacturer disclosure triangulation — Pentair, Hayward, Fluidra all disclose distributor rebate accruals in 10-K segment notes. Year-over-year shifts in rebate concentration could signal POOL vs Heritage share-shift at the OEM tier (already partially captured in

Pool_Distributors_Data.xlsx → Mfr_PullThrough). - Permits → POOL revenue / market-share regression — if Heritage is winning share on price, POOL's local-market revenue should track LESS than 1:1 with local permits in overlap geographies. Requires county-level POOL revenue disclosure, which doesn't exist publicly.

- SRS / Home Depot earnings call mentions — HD's quarterly calls occasionally cite SRS Pool segment performance. Any pricing color from that channel would be authoritative.

- Channel-check more AlphaSense experts — particularly former Heritage / former SRS executives or Pentair regional reps. The current corpus is 2 experts. More gives sharper triangulation.

Methodology & data quality notes

- Heritage data source:

https://www.heritagepoolsupplygroup.com/api/branchList/features/— Next.js API route returning a GeoJSON FeatureCollection (162 KB). No auth, no Cloudflare friction. Reproducible with plain Pythonrequests. - POOL data source: Public locator scrape at

poolcorp.com/map_api/map.php(May 2026), filtered to US only (424 of 476 worldwide entries). - Distance metric: Great-circle (haversine) miles, not drive-time. Underestimates friction in mountain/coastal cases but adequate for ranking competitive proximity.

- Brand mismatch caveat: The API returns 9 brand names while HERITAGE_CONTEXT.md §2 lists ~12 acquired brands. The 12-brand corporate structure is rolled up into the consolidated "HERITAGE POOL SUPPLY" front-end brand in the API. Branch counts are consistent with all acquired brands being included.

- POOL count reconciliation: 424 US locator entries vs 456 sales centers per 10-K (gap explained in HERITAGE_CONTEXT.md §8 — locator excludes some intl, NPT, and recently-closed/in-transit locations).

- Files produced this session (all in

dashboards/pool_locations/):heritage_locations.csv(163 rows) ·heritage_nearest_pool.csv(per-branch nearest pairing) ·heritage_overlap_by_state.csv(51-row state table) ·heritage_overlap_metrics.json(full numeric summary) ·heritage_vs_poolcorp.png(static map) ·heritage_locations.html(folium interactive — embedded above) ·HERITAGE_OVERLAP.md(7-section findings doc) · plus scrapers inscrape_heritage_xhr.py,build_heritage_overlap.py,build_heritage_map.py,build_heritage_html_map.py